- Q2 2023 Net Income – $2.48 million or $0.32 per fully diluted share. Increase of 6.9 percent over Q1 2023

- Cash and securities total $182 million – 18 percent of assets.

- Year over year Net Loan Growth – $160.8 million or 24.4 percent

- Year over year Deposit Growth – $6.6 million or 0.8 percent over June 30th 2022

Summit Bank Group reported net income for the second quarter of $2.48 million or 32 cents per fully diluted share, representing an increase of 7 percent or 2 cents per fully diluted share over the first quarter of 2023. Comparable earnings for the second quarter of 2022 were $3.42 million or 44 cents per fully diluted share. Growth and increased profitability from Summit’s commercial business units improved during the quarter and was accretive to earnings over the same period last year. However, higher loan charge-off activity and losses on sale of collateral in the Bank’s Small Commercial Equipment lending unit reduced earnings per share compared to the second quarter of 2022.

“We were pleased that our margin stabilized during the quarter and that the Bank was able to experience terrific loan growth and modest deposit growth,” said President and CEO Craig Wanichek. “The macro slow-down in the trucking industry had an impact on our commercial equipment lending group, which hampered that division’s results.”

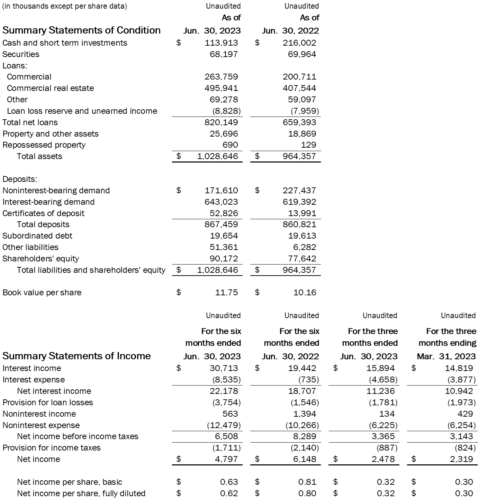

The Bank’s balance sheet has responded well to the rapid increases in market interest rates that have occurred over the last twelve months. Net interest income for the second quarter of 2023 increased by $294 thousand over the first quarter of 2023, an increase of 2.7 percent or 3.8 cents per fully diluted share. Year to date net interest income compared to the similar period in 2022 is up $3.5 million representing an increase of 18.6 percent or 44.8 cents per fully diluted share.

The Bank continues to maintain a highly liquid balance sheet with cash and Available for Sale (AFS) short term securities of $182 million, which represents 17.7 percent of total assets as of June 30th 2023. Additionally, the Bank maintains secured borrowing commitments from the Federal Home Loan Bank and the Federal Reserve Bank with total available borrowing capacity as of June 30th 2023 of $177 million. Combined, the Bank’s cash, AFS securities, and available secured borrowing as of June 30th 2023 total $359 million. This total is 34.9 percent of total assets and 134 percent of total estimated uninsured deposits as of June 30th 2023.

“The Bank is committed to stay in a well-capitalized and liquid position,” said Wanichek. “Summit Bank deposits remain stable despite a challenging deposit environment across the industry.”

Summit Bank’s total non-owner occupied office exposure was just 4.5 percent of total loans as of June 30th 2023 with the majority of such loans in Eugene and Bend. Summit’s two downtown Portland office property loans represent only 0.15 percent of total loans at June 30th, 2023.

Total net loans as of June 30th 2023, were $820.1 million, representing growth of $57.5 million or 7.5 percent during the second quarter and growth of $160.8 million or 24.4 percent since June 30th 2022. The Bank has been successful in retaining client deposits during 2023 with total client deposits increasing by $6.6 million or 0.8 percent and by $10.4 million or 1.2 percent during the trailing twelve months and first six months of 2023, respectively. Return on average equity for the second quarter increased to 11.1 percent from 10.7 percent during the first quarter bringing the year to date figure to 10.9 percent. The Company is currently in its 11th consecutive year producing a return on equity in excess of 10.0 percent.

Growing loans and deposits in a dynamic interest rate environment is the result of Summit’s team working closely with clients. “As we reflect on the second quarter of 2023, I am grateful for our clients and also for our team,” said Wanichek. “Our commitment to providing exceptional service and local decision making to our clients and their businesses and nonprofits has resulted in effective achievements during this period.”

The Company’s strong earnings continue to support its asset growth with total shareholders’ equity ending the second quarter at $90.2 million, an increase of $12.5 million or 16.1 percent since June 30th 2022. The Company’s total retained earnings as of June 30th 2023 has more than doubled during the last three years, increasing by $34.7 million from $28.1 million as of June 30th 2020 to $63.1 million currently.

The Bank continues to hold very low levels of non-performing assets with total non-performing assets at June 30th 2023 representing just 0.13 percent of total assets, up slightly from December 31st, 2022 and June 30th 2022 levels of 0.11 percent and 0.04 percent respectively.

Summit Bank Group Inc., through its wholly owned subsidiary Summit Bank, maintains offices in Eugene, Central Oregon and Portland and specializes in providing high-level service to professionals and medium-sized businesses and their owners. The bank was voted this year as one of Oregon’s “Top 100 Companies to Work For,” according to Oregon Business Magazine. Summit Bank Group Inc. is quoted on the NASDAQ Over-the-Counter Bulletin Board as SBKO.

QUARTERLY FINANCIAL REPORT – JUNE 30th 2023