· Reported record asset-size of $1.08 billion, up 16.0 percent over Q1 2022

· Cash and securities totaled $291.4 million – 27 percent of total assets, an increase of 5.8 percent over Q1 2022

· Year over year Deposit Growth – $108.0 million or 13.0 percent over March 31, 2022

· Year over year Net Loan Growth – $124.9 million or 20.3 percent (excluding PPP loans)

· Q1 2023 Net Income – $2.32 million or $0.30 per fully diluted share

· Opened new office in Westside of Portland

· Purchased building in Redmond for new office

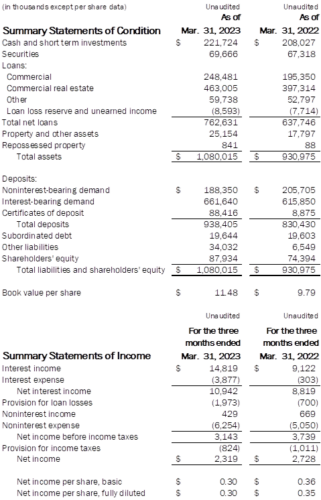

Summit Bank Group (the “Company”) reported significant increased liquidity on its balance sheet during the first quarter of 2023 with $291.4 million in cash and available for sale short-term securities held as of March 31, 2023, representing increases of $16.0 million, or 5.8 percent, and $86.0 million, or 41.9 percent, over March 31, 2022 and December 31, 2022, respectively. The cash and securities position represented 27 percent of the Company’s total assets at March 31, 2023. The conservative securities portfolio consists of US treasuries and US Government backed agency and mortgage bonds. The Bank has remained very cautious over its history purchasing only short-term securities and building a portfolio with an average duration of just 2.3 years.

“We have built a solid and safe balance sheet heading into the remainder of 2023,” said Craig Wanichek, President and CEO. “We have further solidified that position and are situated to continue to grow and take advantage of the disruption in our markets.”

Total net loans as of March 31, 2023, were $762.6 million. Net loans grew by $22.5 million, or 3.0 percent, during the first quarter of 2023 and by $128.6 million, or 20.3 percent, since March 31, 2022, excluding PPP loans. Deposit growth resumed during the first quarter after contracting marginally during the fourth quarter of 2022. Total deposits increased by $81.2 million during the first quarter and increased by $108.0 million, or 13.0 percent, since March 31, 2022. During the first quarter of 2023, the Bank brought on a small amount of wholesale funding to add to its already strong balance sheet.

“We are very pleased with deposit and loan growth during the quarter,” said Wanichek. “The first quarter is typically a seasonally slow quarter particularly for deposit growth. After the challenges the industry faced in March, we actually saw an increase in deposits. The Bank opened a record number of accounts, with no accounts closing due to the industry wide events. Existing and new clients increased deposits or moved deposits to Summit because of constant communication, strong relationships, financial strength and our history of strong results.”

Summit continues to grow its locations to accommodate loan and deposit growth. “The acceptance of our community banking model and the addition of excellent bankers in Portland is very encouraging,” said Wanichek. “As a result, we announced the opening of another office in Portland’s Westside earlier this year. Additionally, due to the continued success of the Central Oregon office, the Bank recently purchased a building in Redmond that will house a new Summit office in the fall.”

Summit Bank Group reported net income for the first quarter of $2.32 million or 30 cents per fully diluted share. Comparable earnings for the first quarter of 2022 were $2.73 million or 35 cents per fully diluted share, representing a decrease of 15 percent to both earnings and earnings per fully diluted share. Higher loan charge-off activity in the Bank’s Small Commercial Equipment lending unit reduced earnings per share during the first quarter compared to the first quarter of 2022. This negative impact was mitigated by growth and improved profitability from Summit’s other banking units.

The Bank continues to hold very low levels of non-performing assets with total non-performing assets at March 31, 2023 representing just 0.12 percent of total assets, up slightly from December 31, 2022 and March 31, 2022 levels of 0.11 percent and 0.05 percent, respectively.

“Our small equipment commercial lending unit is experiencing a higher level of losses, but remains accretive to earnings,” said Wanichek. “The traditional banking units’ credit continued to perform at an extremely high level, experiencing little to no loss activity.”

Summit Bank’s office exposure was 10.3 percent of total loans with the majority of such loans in Eugene and Bend. The two downtown Portland office properties represented only 0.14 percent of total loans at March 31, 2023.

Return on average equity for the quarter, while reduced compared to 2022, was 10.7 percent. The Company is currently in its eleventh consecutive year producing a return on equity in excess of 10.0 percent.

The Company’s strong earnings continue to support its asset growth with total shareholders’ equity ending the first quarter at $87.9 million, an increase of $13.5 million or 18.2 percent since March 31, 2022. The Company’s total equity capital as of March 31, 2023 has increased by $39.6 million from $48.3 million at March 31, 2020, resulting from a combination of a successful common stock offering during the pandemic period and $33.7 million in retained earnings over the three-year period. The Bank also advanced $25 million on its FHLB line, a conservative move, in light of the current environment.

Summit Bank Group, Inc.

Summit Bank Group Inc., through its wholly owned subsidiary Summit Bank, maintains offices in Eugene, Bend and Portland and specializes in providing high-level service to professionals and medium-sized businesses and their owners. Summit Bank is a recipient of this year’s 100 Best Places to Work for in Oregon and 100 Best Green Workplaces in Oregon. Summit Bank Group Inc. is quoted on the Over-the-Counter Bulletin Board as SBKO.

Forward Looking Statements

This press release contains certain forward-looking statements about the Company and the Bank. Forward-looking statements include statements regarding anticipated future events or results and can be identified by the fact that they do not relate strictly to historical or current facts. Forward-looking statements, by their nature, are subject to risks and uncertainties. Certain factors that could cause actual results to differ materially from expected results include increased competitive pressures, inflation, changes in the interest rate environment, general economic conditions or conditions within the securities markets, potential recessionary conditions, changes in asset quality, charge-offs and loan loss provisions, changes in demand for our products and services, legislative, accounting, tax and regulatory changes, including changes in the monetary and fiscal policies of the Board of Governors of the Federal Reserve System, the continuing impact of the COVID-19 pandemic on our business and results of operation, political developments, uncertainties or instability, catastrophic events, acts of war or terrorism, natural disasters or breach of our operational or security systems or infrastructure, including cyberattacks that could adversely affect the Company’s financial condition and results of operations and the business in which the Company and the Bank are engaged.

Accordingly, you should not place undue reliance on forward-looking statements. The Company undertakes no obligation to revise these forward-looking statements or to reflect events or circumstances after the date of this press release.

QUARTERLY FINANCIAL REPORT – MARCH 31, 2023